Help – My Accountant & Bank Manager Aren't Speaking the Same Language!

Cash, Accounting, Profit & Taxable Profit

When it comes to working out the difference between your accounts for your franchise business and your bank balance, it sometimes seems that everyone is talking a different language – potentially none of which you fully understand!

Accountants quite often talk about cash, profits, accounting profits, and taxable profits all in the same sentence, but you may be asking yourself: “Isn’t that all just the same thing? And, if I have cash in my bank account, doesn’t that mean that I’ve made a profit and I can just spend it?”

Your accountant might be saying one thing about your money, while your bank manager is saying something quite different!

So, how do you know exactly how much money you’ve made at the end of every tax year?

It’s all in the timing, and here’s why…

The cash in your bank account is made up of receipts from customers and payments to suppliers, but how much you have in profit at the end of each tax year depends on when money moves in and out of your bank account.

So, let’s start with profits – sometimes called gross profits and net profits.

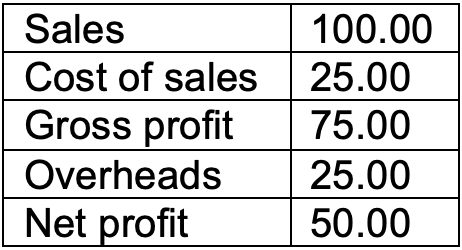

Gross profits – what are they?

Sales – cost of sales = Gross profit

The cost of sales is the direct cost of materials or effort used to make the product or service your franchise is selling. For example: if you’ve made a cake to sell then the cost of the sales would be the ingredients – the eggs, flour, sugar, and butter.

So, if you’ve sold a cake for £100 and the ingredients cost you £25, then the gross profit would be £75. So far so simple. You’ll also have incurred some overheads along the way, which might include things like renting a kitchen, electricity, or gas to power the oven, etc. You might also have purchased stationery or paid for advertising, and so on.

Net Profits – what are they?

Gross profit – overheads = Net profit

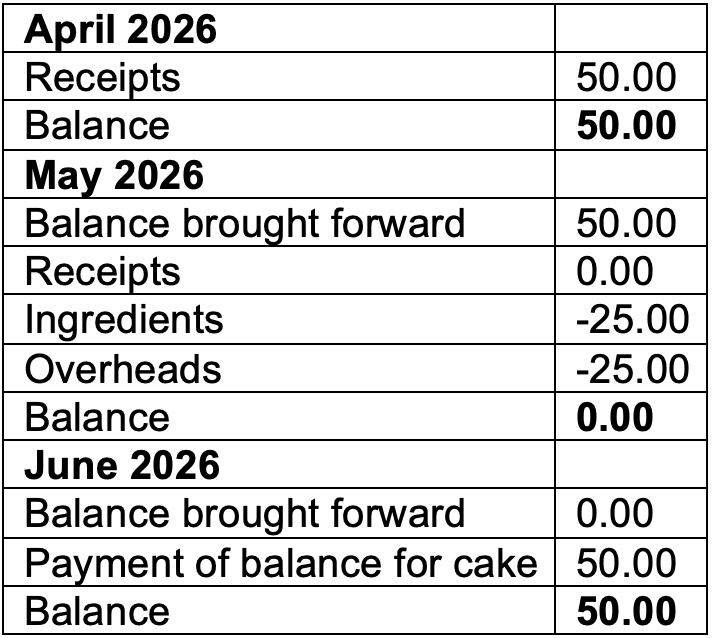

Profit is different from cash because of timing. Profit is calculated based on the invoice date. For example, you raise a sales invoice to a customer dated 15th May 2026 for a cake costing £100.

Here’s what a simple calculation in your accounts would look like:

Profit for May 2026

Now, your bank balance may look very different, depending on the timing of when money was paid, and which direction it goes in.

Let’s further the example to explain this.

The customer paid a 50% deposit in April when they placed the order but didn’t pay the balance until June. So where does that leave your accounts? Let’s have a look at your bank balance just for that one bit of business over those few months.

It looks quite different to your accounts:

So, as you can see, in May 2026, although you were paid £50.00 and your bank balance showed a net profit (or accounting profit) of £50.00, you had nothing in the bank, as the customer hadn’t paid the full amount for the cake.

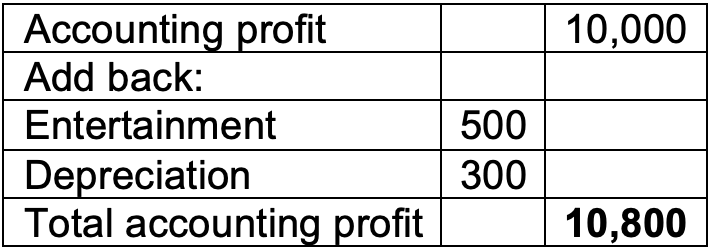

When your accountant prepares your accounts, they’ll calculate the net profit and will most likely refer to this as the accounting profit – this is the profit before tax, which is carried forward onto next year’s accounts.

Certain adjustments then need to be made before arriving at the taxable profit. For example, you might have tried to claim for the cost of entertaining a customer, only to be told by your accountant that the expenditure is not allowable for tax purposes.

To remedy this, at the end of the year your accountant will add back entertainment costs before calculating the tax due, which looks something like this:

Allowances – depreciation, capital, and costs

Now, let’s imagine your franchise business is doing well and you decide to scale up.

During the year you buy some equipment, sometimes referred to as plant or machinery. These are classed as long-life assets as you’ll be using them over a series of years. They’ll go on the balance sheet as an asset of the business, rather than a cost on the profit and loss account.

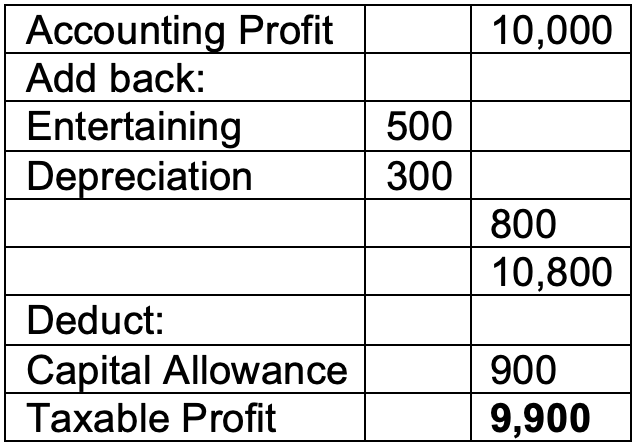

Costs are things that will be used up – ingredients, stationery, etc. As for your larger items – your assets – your accountant will most likely depreciate your assets over 3 or 5 years. That depreciation – a portion of what the equipment cost – will be tallied on the profit and loss account and be included in the accounting profit.

When calculating the taxable profit, your accountant will add the depreciation back into the accounting profit. This is because everyone calculates depreciation differently, so it wouldn’t be fair if tax were to be calculated on a figure arrived at using different methods.

So, instead of depreciation, your accountant will claim capital allowances, which are prescribed by the government. Beware though, at Budget time rules can always change, so make sure you keep on top of what’s allowable.

Currently, the annual investment allowance remains at 100% for capital investment up to £1m. So, say for instance you buy a laptop for £900, your accountant may depreciate it over three years, but you’ll most likely get 100% relief in the tax computation at the end of three years.

It may look like this:

It may seem a little complicated to get everything straight in your mind in terms of what’s allowable and what isn’t, especially if you’re new to accounts, but there are two things that will help:

A supportive and communicative accountant is worth their weight in, well, gold! Make sure they’re able to understand your franchise business and interpret accountancy jargon for you, so you’ll know your profit from your loss, and your capital from your costs from the get-go.

If you’re keeping records yourself, start as you mean to go on. Make sure you keep on top of your money, where it’s going and what’s allowable, and you’ll have a stress-free tax assessment.

If you’d like more help with demystifying your accounts, from accountants who understand the franchise business inside and out, we’re here to help. DOWNLOAD OUR FREE EBOOK, ‘Why Every Accountant is NOT the Same – and Why That Matters for Your Business’ and then get in touch.